However, only a few months later and the chance to play to the gallery of popular public opinion proved too tempting as the Conservative Party entered its annual conference season. Although highly regarded for her cautious approach to party politics, Prime Minister May decided to use the speaker’s platform to indicate a tough stance on immigration, the banking sector and even suggested a wide ranging break with Europe’s common market.

Seasoned commentators had expected some grandstanding as the Conservative party fights hard to win back voters from UKIP (United Kingdom Independent Party). However, the subsequent 6 percent drop of pound sterling against the dollar within one day only left many fund managers worried that recent comments by the Prime Minister may push the currency further downward over the coming months.

During recent trading sessions a large number of investors have also began to focus on cautionary comments coming from Nissan and other Asian companies on possible scaling down of their UK investment plans. This area is being closely watched because of Britain’s heavy reliance on FDI (Foreign Direct Investment) to balance its books.

Even if pound sterling should fall further, the FTSE100 may well continue to rally due to overseas earnings of companies included in the index. On the other hand, an adverse impact on imports could make British consumer’s confidence evaporate quickly. As we all well know, politics is an art – a delicate balancing act between competing interests.

From our side, we are hopeful that the UK negotiating team will take a more pragmatic approach behind closed doors.

At the moment, all eyes are on the forthcoming US elections in November.

Meanwhile, unemployment rate rose to 5 percent in September compared to 4.9 percent in the previous month. Latest statistics of new jobs creation show an average growth per month in 2016 of 178,000 indicating a slight slow-down from 229,000 in 2015. The messages from the labour market lowered somewhat expectations of the FED raising interest rates shortly.

Of greater importance is the potential interest rate rise in December, which has been well telegraphed by the Federal Reserve, as well as the further interest rate hikes in 2017 which are very likely to be modest.

Accordingly, it is expected that any asset class without excessive risk and offering uplift in income versus cash, will still be in demand as we proceed into the next year.

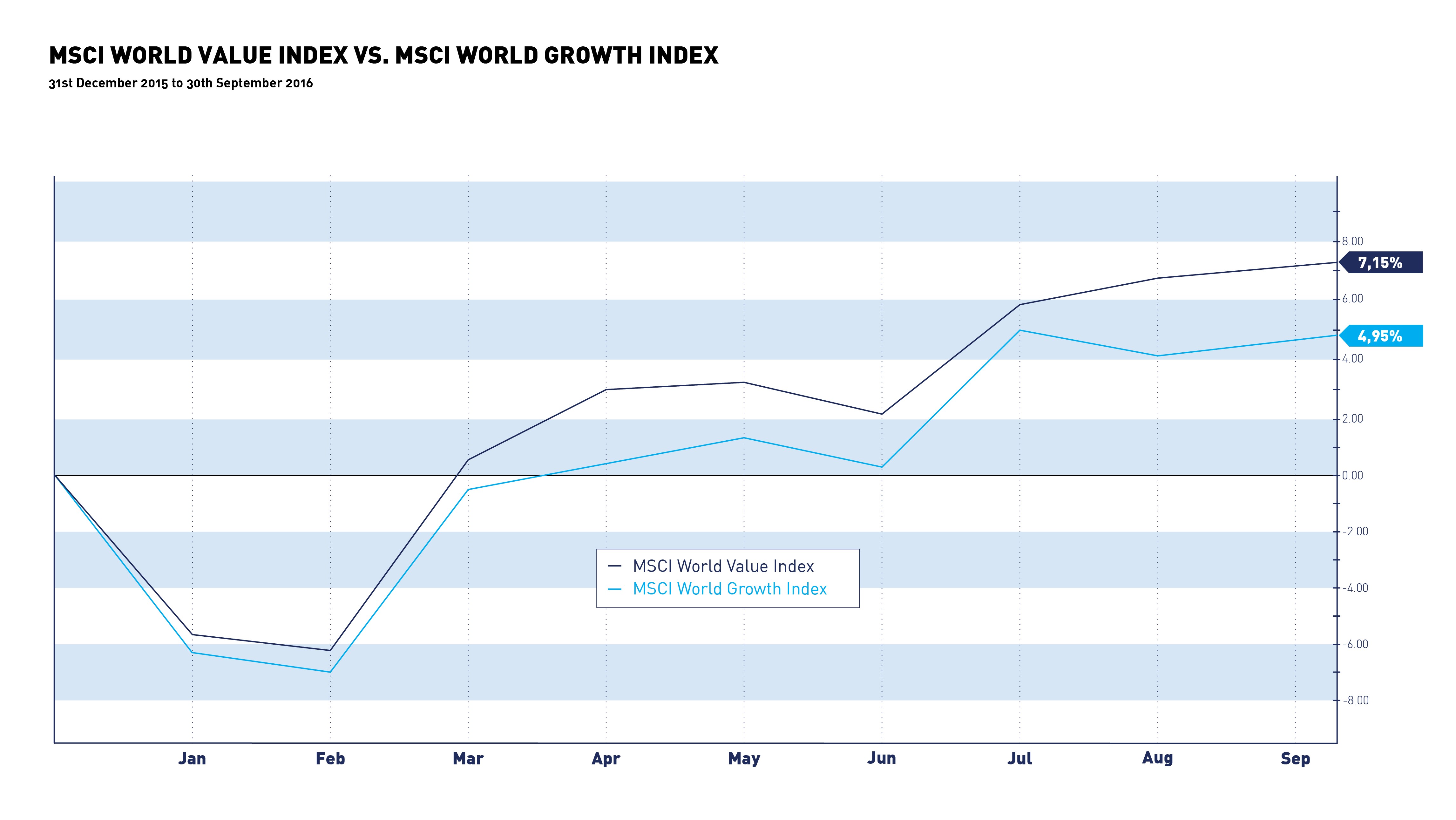

Memories of the great financial crash of 2007/8 and the subsequent contraction in PE ratios for numerous growth stocks are still relatively fresh among investors. Since the growth stocks have in fact performed well in recent years, it is interesting to note that value based stocks have outperformed growth orientated equities so far this year.

This should perhaps come as no surprise. Investors are becoming slightly more wary of paying too much for growth, and the Price to Earnings Growth figure, also known as the PEG ratio, is still a popular filter for many fund managers.

As measured by the MSCI World Equity Growth index, the growth equities are estimated to be trading on a forecast PE of 19.4x for 2016, while value stocks are trading on 15.6x. However, this still begs the question: What has happened in the market to improve sentiment towards this market segment?

Value based investors have started to look again at the commodity & energy sectors, as there have been tentative signs that China will not slow down as badly as previously feared. In addition, there have been more soothing noises from OPEC following the first supply reduction in eight years and Saudi officials are now talking up the prospect of oil at 60 dollars for a barrel by the end of the year. This type of news flow is undoubtedly helpful to the oil and energy sector, which has been cutting back on its workforce and capital investments for a long period of time.

Elsewhere, price conscious investors are also beginning to cast their eye once more on US and European bank stocks where a combination of low net interest margins, increasing capital requirements, and a steady flow of high profile regulatory fines has eroded confidence in the sector. Whilst it is difficult to be very positive about the banking sector, on various measures most valuations score at the lower end of their historical ranges.

Aside from the obvious PEG rules, investors still seem keen on looking for strong business franchises, modest amounts of debt to equity ratios, and of course strong free cash flow. While it is always good to see strong cash flows within each business, there are increasing signs that investors are also looking for catalysts of change such as new incentivised management teams and shifts within the shareholder register.

In the case of the latter, we have noted some evidence of stake-building within some well-known European stocks, while US based value driven investors begin to make their presence felt.

Your Wealth at a Glance.

{kind=link}