Please read on for hopefully a different easily understandable and refreshing viewpoint

For the first time in almost a decade we have temporarily reduced our equity weighting in discretionary portfolios towards the neutral zone from an overweight stance.

Whilst we still don`t subscribe to the consensus view that we are in the latter stages of a cyclical bull market ( we still believe there there is significant room both in terms of duration and percentage gains for much longer than most anticipate) there are some current issues which give us pause.

The recent threat of tariffs (now removed) on Mexico by the USA for purely political (immigration) purposes not related to economics has we believe led to an increased weaponisation of the tariff tool. The fact that this move led to no censure of the President by either Congress or the Republican party really gives us cause for concern that Presidential powers remain unchecked (rather dangerous in a democracy).

The recent loud calls for interest rate cuts by the Federal Reserve (by TWEET) and the talk of a demotion of the head of the Federal Reserve to be replaced by someone who presumably who will do what is told again sets up a very dangerous precedent of undermining the indepedence of the largest central bank in the world.

We are also concerned about the use of tariffs on named currency manipulators (currently going through the consultative process) as this lead to another area of uncertainty.

To put it in simple terms think of the walking paterns of a toddler which are highly unpredictable and erratic. This pattern in equity markets makes us nervous – we have no problem in taking risks if the odds are in our favour however with so much depending upon binary outcomes at the moment the odds of 50/50 on many major issues make us cautious and leads us in the short term to have less conviction.

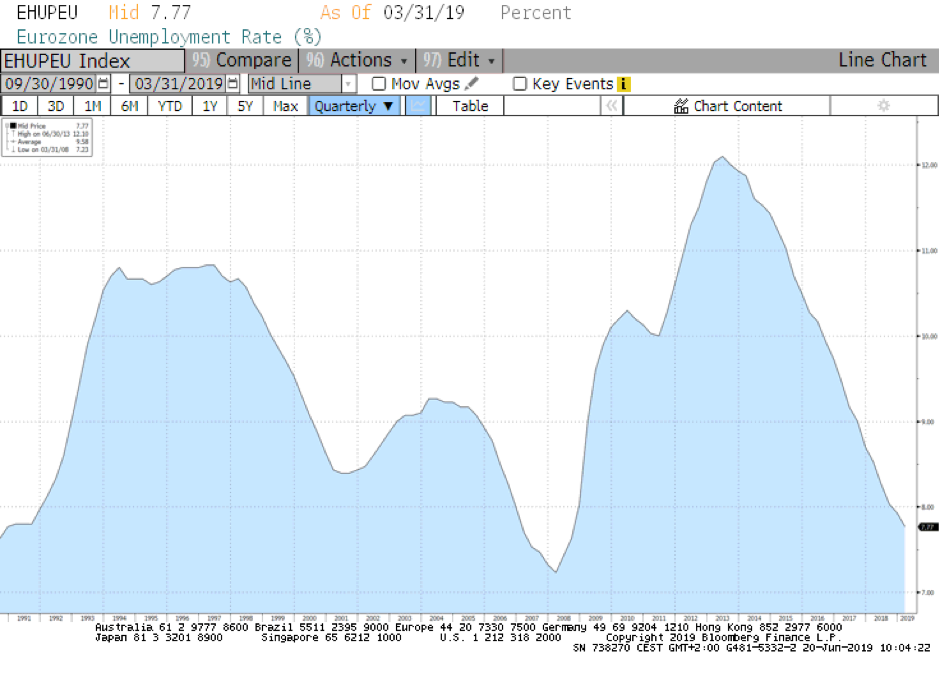

Consumers remain strong and are still spending probably due to low unemployment rates both in current and historic terms

In fact even though it has gone unnoticed by most even in Europe the trend is looking encouraging

Whilst there willundoubtably be a slowdown both in the global economy and the US economy (mainly due to companies reigning in capital expenditure plans due to uncertainty) we still see no recession. The recent moves by central banks- Federal Reserve possibly opening the door to a rate cut in July and the premptive moves by the Chinese central bank and government of tax cuts, infrastructure spending and stimulus for the auto industry should help soothe the negative effects of the tariff uncertainty. The European Central bank has also been active verbally in pushing the notion of further negative rates and despite Mario Draghi`s tenure coming to end in the not too distant future don`t be surprised by a last salvo (perhaps the reintroduction of quantative easing).

Whilst we are still frustrated that global economies are growing below their potential there is still scope for this situation to be rectified.

Especially if you have underestimated the size and resolve of your adversary. Whilst we do not expect a full trade deal at the G20 meeting we think there is a distinct possibility of the next round of tariffs being put on hold whilst discussions between the US and China take place.

We strongly disagree with the notion that this is a long drawn out trade/ tech war which will not be resolved for decades (although this makes great headlines and is now a consensus view). The reality is in fact probably much more simple and could lead to an agreement by year end.

Looking at the recent nuances and putting them into simple terms it is rather like a first date when phone numbers are exchanged. You wait for the phone to ring but if it doesn`t do you call?

It is telling that the US picked up the phone to China to arrange the meeting between the two leaders at the G20 summit. What is also telling is that the previous rhetoric of there would be no trade deal without adhering to the US previous demands has changed. At Trumps`s formal re election rally in Florida this rhetoric has been dialled back to a fair trade deal with China.

Of course there is still the issue of Huawei but once again we beg to differ from the consensus. We do not really believe that the US President is actually a China hawk but he may however give off that vibe to acheive his objectives. He is first and foremost a businessman and everything is negotiable and he has shown time and time again that he is willing to ignore almost everyone if it acheives his objectives.

The clock is ticking and with the US elections just under one year away an economic recession would not be a great vote winning strategy. Time is also running out on delivering on election promises with only a South Korea trade deal signed so far. The next round of tariffs on China would be felt more acutely by the US consumer who could then possibly reign in spending.

Maybe however we should look to the precedent of what happened regarding the steel and aluminium tariffs. Europe reacted in a fast and coordinated way (trade is about the only thing that Europe has a consensual opinion on) specifically and ruthlessly targeting areas of Trump`s core base of supporters (Harley Davidson, agriculture, peanut butter, bourbon etc). The European trade comission has already stated that the retaliatory tariffs are ready to go should the US proceed with their auto tariff threat.

In fact according to the office of the United States Trade Representaive Europe if taken as a whole ranked as the most important export market for the USA in 2018 with goods and services trade totalling nearly USD1.2 trillion in 2018 accounting for nearly 20% of the US total exports and supporting over 2.6mn jobs.

Of course everything could change with one late Sunday evening tweet.

Taking some steps back and gaining perspective we should be greatful for the environment we live in. We are unlikely to see its like again!

Peter Ahluwalia, Chief Investment Office, Partner

peter.ahluwalia@swisspartners.com

Your Wealth at a Glance.