“Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria. The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.” – Sir John Templeton

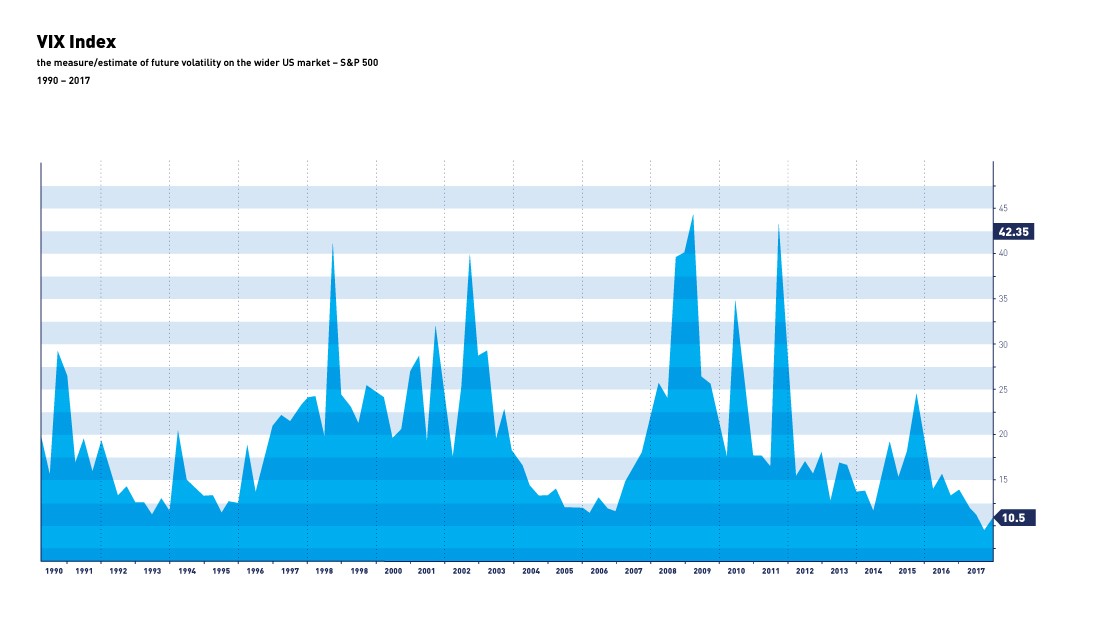

Looking at the relatively low level of volatility in US equity markets as measured by the VIX index, many observers remain concerned that investors have become complacent and that we are nearing the end of this cyclical (read 7 to 8 years) bull market in stocks. An alternative explanation for the depressed level of volatility in markets could well be that the rise of passive investing (following indexes), computer driven strategies, Central Bank interventions (QE) and alternative strategies, like selling volatility, have all contributed to this current repression of volatility in equity indices.

Interestingly, volatility at the individual stock level has remained relatively high with 10% plus daily moves in “blue chips”, not an uncommon occurrence, perhaps again partly due to the rise of passive investing and the decline in number of active investors (stock pickers). This can lead to interesting opportunities for those who are prepared to swim against the tide.

Markets have continued to grind higher despite many short-term challenges such as the bellicose rhetoric between the USA and North Korea, which we view as continuing in its current form with only the slight chance (let`s say 5 to 10%) of something disastrous happening.

The recent turn of events in Catalonia has unnerved investors and caused some short-term underperformance of European stocks versus their US counterparts with some now talking about the Italian regions of Lombardy and Veneto wanting to separate from Italy. Of course, if we carry on this line of thought, none of Europe is safe, and even Bavaria has regularly complained about the high financial contribution it has to pay to Berlin.

It`s definitely time for a reality and fact check. In the recent (illegal) Catalan referendum, only 43% of the population turned out to vote and out of those 90% voted in favour of independence. This represents under 39% of the overall Catalan voting population – hardly a clarion call to the founding of a new, independent Catalonia. The likely scenario now is that autonomy from Madrid will be taken away temporarily until new regional elections are held, which is probably the only course of action the Spanish government can realistically take.

Rhetoric between both parties will no doubt remain heated. Facing Europe`s already quick refusal to recognize the referendum result, Catalonia’s large reliance on the EU and on Spain (65% of its exports go to the EU and more than 35% to Spain), and the very real danger that many businesses will relocate to other parts of Spain (some have already done so recently), makes it seem on the outer realms of possibility that an independent Catalonian state would succeed. Moreover, if Catalonia were independent its debt ratio would rise from its current level of 33 to 100%, to which Catalonia’s share of Spain’s debt would have to be added. Not to mention that an accession to the EU would have to be approved by all EU Member States, including Spain

Flipping back to the opening quote of this newsletter, it would seem pretty evident that we are not at the euphoric stage of this bull market, and a convincing argument could be made that we are still in the sceptical stage, i.e. 50% of the way through with plenty of room left to run.

Your Wealth at a Glance.

{kind=link}