Our decision to decisively increase equity exposure in the eye of the storm seems to have been well timed, as markets posted a spectacular recovery, while the doomsayers were once again proven wrong.

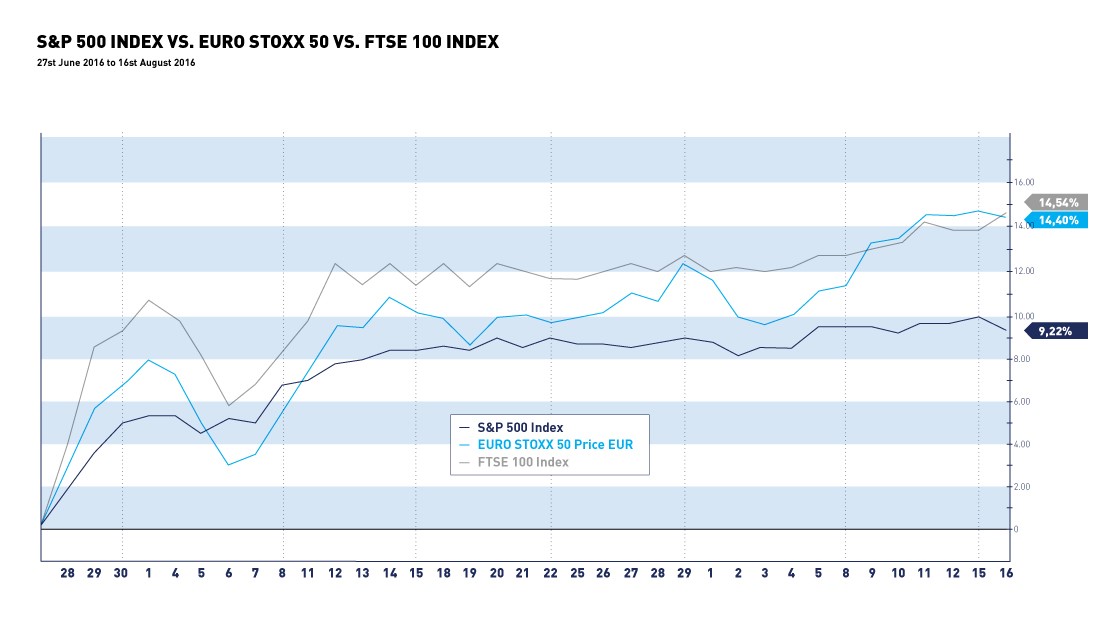

European markets made most headway but still have a large catching up to do compared to their US peers. At this point in time European markets as measured by the Eurostoxx 50 index are still down -4.4% for the year, whilst US equities as measured by the S&P500 are up 8% over the same period.

The gap of underperformance by European equities versus their US counterparts is closing; nevertheless, we expect much more progress before year’s end. With European equities trading on a price -earnings ratio of 14x this year’s earnings versus 18.5x for US equities, the valuation gap just looks too wide. A compelling argument on valuation grounds can also be made when looking at the relevant risk free rate (the 10-year sovereign bonds yield). European equities yield 4% versus the 10-year German Bund yielding -0.04%, whilst US equities yield 2.11% versus the 10-year Treasuries yielding 1.58%.

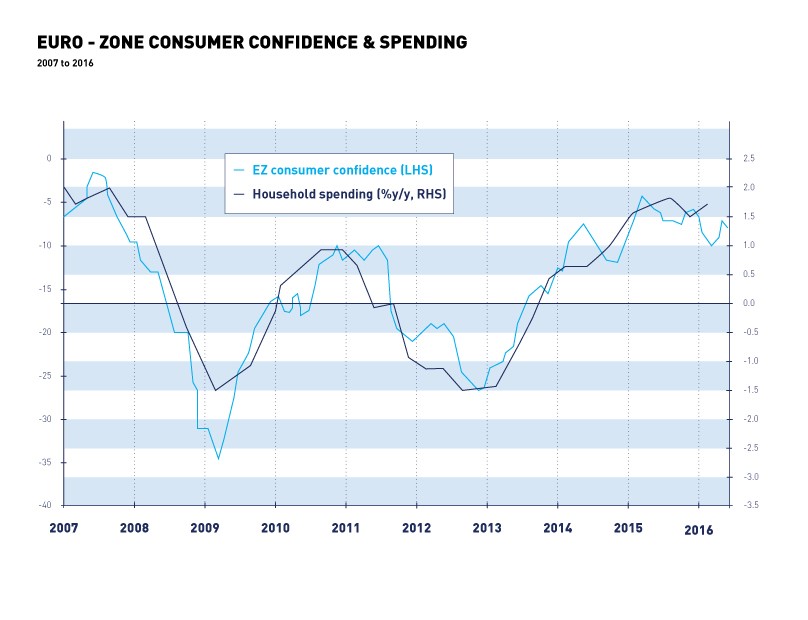

We realise that we are in a very small minority against the consensus by being overweight in European versus the US equities, however, we see signs of encouragement. European consumer confidence and spending has held up well post BREXIT and there are also signs of the UK car market resiliency – a market important for the EU carmakers.

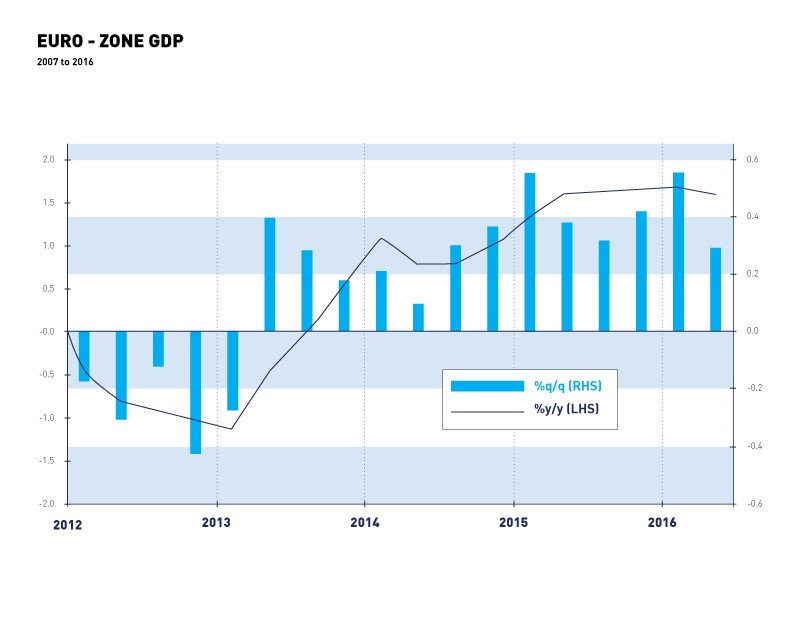

Eurozone growth has also held up well despite the many dire post BREXIT predictions. Furthermore, with the recent discouraging GDP figures from the USA the GDP growth differential has narrowed substantially.

Looking at the latest Bank of America Merrill Lynch surveys it seems that recent cash holdings by investors have been reduced substantially (they were at record highs post BREXIT) with a strong bias towards an overweight in US equities. These are the same investors who escaped into cash in the February market drawdown but were bullish after the recovery.

We will continue with our old fashioned approach of trying to buy low and sell high.

Whilst we still find value in some selected US equities, we find significantly more in the blue chip European companies with global businesses.

I leave you with the thought that the most money is made in markets by not following the consensus opinion.

Your Wealth at a Glance.

{kind=link}

{kind=link}

{kind=link}