Since we last elucidated these thoughts, many market participants have come around to our way of thinking and this makes us decidedly nervous as it is not always good to be part of the crowd or the consensus.

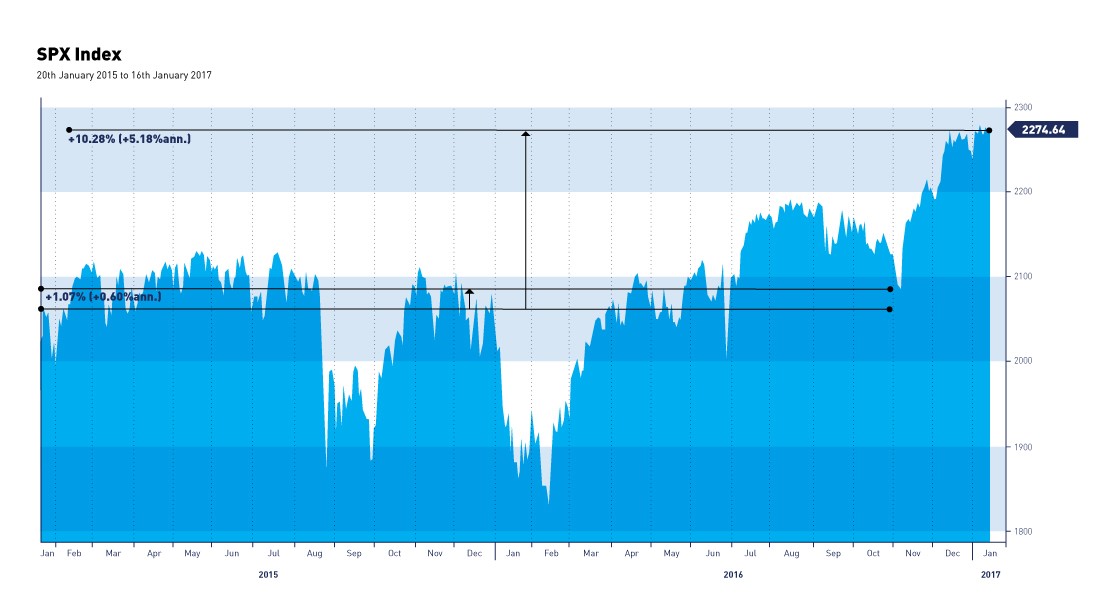

Looking at the progress the S&P 500 has made over the last two years until the US election, the gains have been incredibly muted (essentially flat). In principle the US market has broken its sideways movement of the last two years since the election, and whilst in the very short term the gains may seem too sharp, they remained in fact rather moderate over the last two years.

Whilst trailing valuations on the S&P500 don`t look cheap at 21x next year`s, valuation at 15x looks much more reasonable.

So where does this leave us? In short term the US equity market could be vulnerable to disappointments over promised fiscal measures. However, market corrections can happen in various formats- sector rotation we have seen some of this already), or the market could just move sideways .

One thing does seem pretty certain and that is that volatility is likely to increase. Making your portfolio “tweet proof” could be an interesting strategy for the US and global investors this year. You just have to look at the price movements of traditional Swiss pharmaceutical stocks to see that we are not in a normal environment. Sectors that seem to be exposed to this phenomenon are bitotechs/pharmaceauticals, defense and car producing companies.. Whilst banks have remained relatively immune, we guess that this could be about to change. To try and “tweet proof” your portfolio you need to think in populist terms. The perception of the average US consumer is that drug prices are too high. When looking at banks we believe the average US person believes they are making too much money, especially after what happened in 2008. Therefore, “tweets” about the banking sector would be a victimless crime (except for the banks) and would be populist in their nature. Sectors which have remained relatively immune are technology, media and commodities.

There has been a lot of speculation about whether US bonds are now in a bear market. The trick with surviving bear attacks is figuring out what kind of bear it is that is attacking you – a teddy bear – hardly the stuff of nightmares, a koala bear – more vicious than they look, they have sharp claws, or a grizzly bear – most likely fatal.

Given that we have been in a multi decade bull market for bonds, we expect the decline to be perhaps more gradual than many think. In our opinion a bear market in US bonds would be confirmed by the 10-year pushing through the 3 percent level and the 30-year breaking the 4 percent level. These were the old 2013 taper tantrum yield highs.

One must also be cognisant of the fact that the largest holder of US Treauries is actually the US Government, and that with the large amount of US debt every increase in interest rates increases the amount the Government has to pay to service its debt.

Your Wealth at a Glance.

{kind=link}