The recent decision by the UK to leave the European Union has caused considerable turbulences in the markets in the short term. However, given the fact that Article 50 of the Lisbon Treaty has not yet been invoked, and may even be delayed until next year, we see no reason to despair over the World economy exiting its growth phase (WEXIT). In fact, in legal terms, and for the time being, not much has changed – the UK still remains a full-fledged member of the EU. Furthermore, it is likely, that before invoking Article 50, it will have to be debated in the House of Commons and the House of Lords, with a possibility of overturning the referendum decision, if both chambers of the British Parliament agreed. Therefore, if and when Article 50 is invoked, it is important to sift through the economic implications of this act.

The UK is likely to feel most of the impact, and we have already seen this in the currency adjustment – the fall of GBP. This phase may not be over yet, as interest rate cuts and expansion of QE (quantative easing) by the Bank of England are likely to be needed to cushion the impact of higher prices of goods and services, and also to possibly deal with trade tariffs imposed in the future. The twin deficits in the UK present yet another problem.

Europe will be less affected; however, Eurozone’s growth is likely to slow down by 0.3% to 0.5% over the next 18 months, remaining nonetheless positive. Within Europe the German economy is most likely to feel the impact due to its large car exports to the UK. The US economy, by and large, will probably not suffer at all, however, it is important to keep an eye on the UK banks, considering that the US banks are highly exposed to the UK banking industry – much more so than the European banks.

No one till now has really explained, what BREXIT could mean in detail. Think of it as three different flavours – BREXIT light, medium and full fat.

Light – would entail still trading with the European Union in a tariff-free or a very low-tariff mode, medium – would be less beneficial, and full fat – would mean reverting to the WTO terms of trade. The early indications are that we are heading towards the light flavour of BREXIT.

We felt that the initial turbulences after the UK referendum result were too extreme. Therefore, we increased equity exposure (to blue chip companies) by 3% in conservative mandates, 5% in balanced, and 7% in dynamic mandates, primarily to European companies doing business on a global basis.

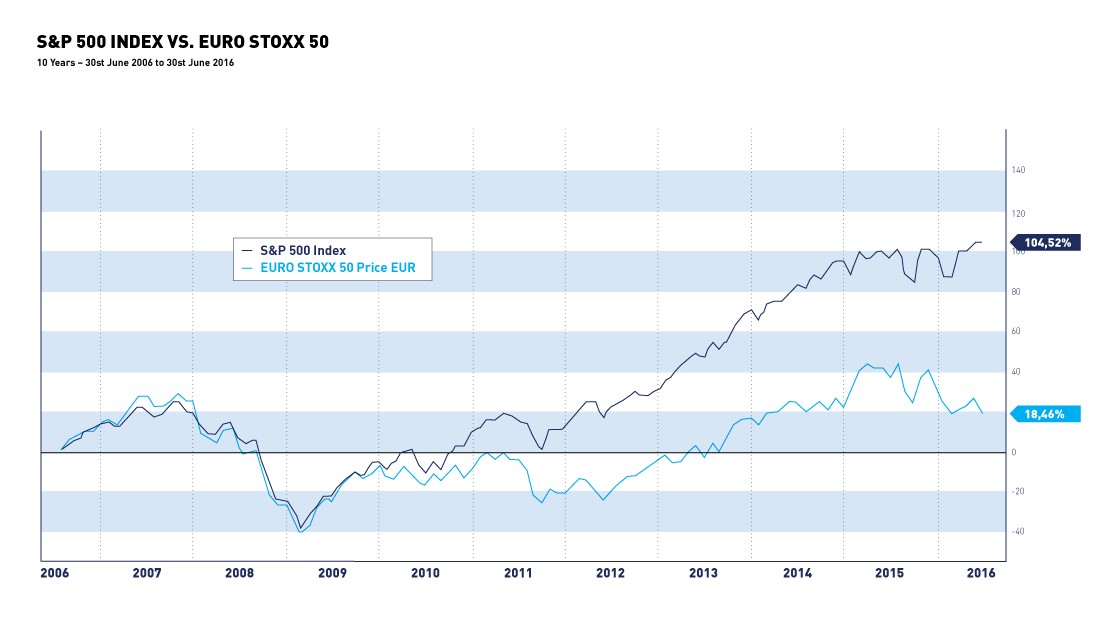

At this point in time we feel, that European markets look severely undervalued compared to their US counterparts, while the levels have reached an extreme and not sustainable territory.

GDP growth in Europe is likely to catch up with that of the US, or rather the gap will narrow. Earnings estimates for European companies are now at a seven-year low. Post BREXIT strategists are in a deeply bearish mood; they have gone over the ten-month period from forecasting a 10% gain for the Eurostoxx 50 at the beginning of the year to a 10% decline now. We have seen twenty two weeks of straight outflows from European equity fund – the worst since 2008. Everyone seems to be waiting for the next domino to fall, which we believe will not happen. The US economy is likely to carry on in its stop-and-go manner, and we expect US equities to perform ok. The upcoming earnings season has the bar put so low, that it would be difficult for companies not to beat such low expectations.

GDP growth in Europe is likely to catch up with that of the US, or rather the gap will narrow. Earnings estimates for European companies are now at a seven-year low. Post BREXIT strategists are in a deeply bearish mood; they have gone over the ten-month period from forecasting a 10% gain for the Eurostoxx 50 at the beginning of the year to a 10% decline now. We have seen twenty two weeks of straight outflows from European equity fund – the worst since 2008. Everyone seems to be waiting for the next domino to fall, which we believe will not happen. The US economy is likely to carry on in its stop-and-go manner, and we expect US equities to perform ok. The upcoming earnings season has the bar put so low, that it would be difficult for companies not to beat such low expectations.

Essentially we are buying great assets at sale prices.

With the strong win of Abe in Japan, there has been much talk of helicopter money – the central bank printing money and giving it to the man in the street or to the government for fiscal stimulus. Given the length of time that the Japanese economy has been in the doldrums, drastic action is needed. Think of it as microlite money at first. I expect the BOJ to conduct monetary stimulus in coordination with a fiscal stimulus from the government – tax cuts, infrastructure projects etc. This is the first step towards helicopter money, which could eventually come. Other central banks would be watching with close interest. Should the experiment succeed, it will be likely adopted by the ECB and then by the US FED. It is worth to remind here, that an almost USD 5 trillion of monetary stimulus by the US since the global depression, resulted in a GDP growth of merely 2%. If the world goes down this route, then equities (and perhaps gold) are likely to be the major beneficiaries, as inflation sets on an upward path. Bonds, especially the longer dated ones, will suffer terribly.

Bonds do raise our concern, now that we are in the situation of having USD 17.5 trillion in bonds with negative yields. Even the CHF 50-year bond went negative recently! At some point yields will have to rise, and a lot of investors will get hurt. We have kept our bond maturities short and our positions very well diversified in order to protect clients rather than reaching for yield, which we consider dangerous at this point. The alternative segment in our portfolios has done well and has cushioned us somewhat from the recent market turbulence.

– Written by Peter Ahluwalia

Your Wealth at a Glance.

{kind=link}