The forthcoming US mid-term elections are scheduled for 6th November 2018 and will undoubtedly be an important factor to watch in the coming weeks.

Opinion polls can of course be quite misleading as voters stated intentions do not always translate into an actual decision to make the journey from their homes to the ballot box. As usual, the result will depend greatly on the number of Republicans and Democrats who feel ‘fired up’ enough to vote on the day. The battle between the two opposing camps is becoming interesting as both Republican and Democrat party bases seem more engaged than usual.

A closer inspection reveals three populist concerns on both sides. The common issues include immigration, the perception that the rust belt states are being ‘left behind’ by the coastal elites, and of course gender politics.

Current readings from respected American commentators suggest that there is perhaps a 60% chance that the Democrats will take the Lower house, whilst the Republicans will maintain control of the Senate.

For financial markets on the day after the elections, the focus will be on whether Trump has been de-railed. For example, if the Democrats win both houses they may feel emboldened enough to start impeachment measures against Mr Trump. However, as we witnessed with Clinton during the 90’s impeachment measures can backfire and make your own voters more determined than ever to rally around their leader.

Even if Trump was impeached due a major fresh scandal, Mr Mike Pence could quickly step in to fill his shoes and the stock market may actually rally on the news as the Vice President is credited as being perhaps less volatile in nature.

Looking further down the line towards the next Presidential election, it seems clear that Trump is becoming hard to stop. It may take a series of very witty and perhaps waspish final ‘put downs’ during a televised debate or perhaps a fresh Republican scandal before the Democrats feel they have regained any sort of momentum.

A quick look at the current list of Presidential hopefuls from the Democratic Party seems to leave most of the party faithful feeling un-inspired.

However, not all is lost for the ‘Left’ in America as Californian Senator Kamala Harris is popular with voters and of course, there can always be surprises. After all, not so long ago Obama came from nowhere to win the Presidency.

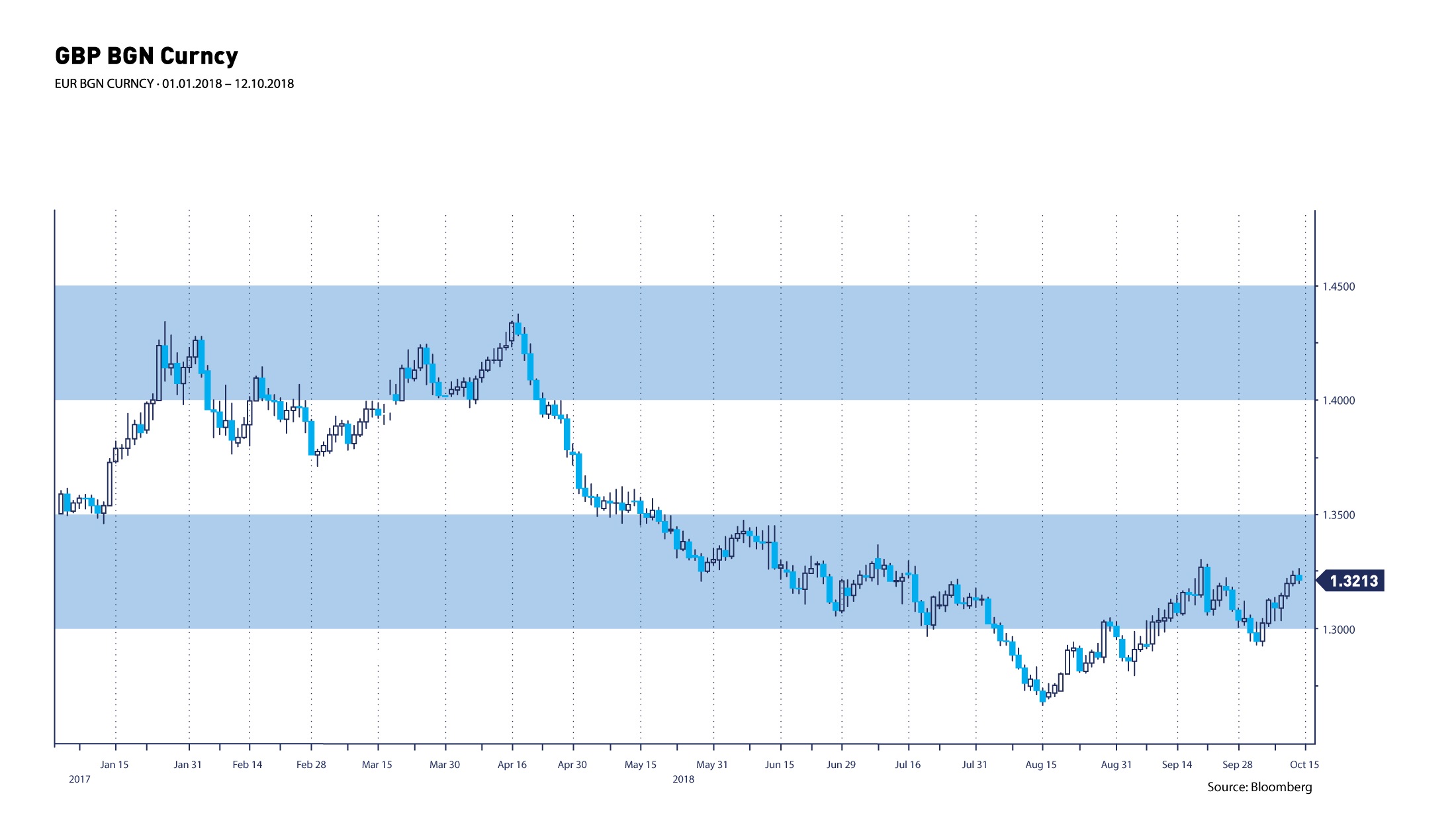

Current indications from the Brexit discussions suggest that Britain is edging closer to a deal with Europe on the terms of its departure. Hopes that a deal would be completed have been clearly visible as sterling rallied against both the US Dollar and the Euro in recent weeks.

Prime Minister May has a number of highly respected business advisers around her – some of whom are well removed from the public eye. However, they do understand the fundamental need for Politicians to keep Britain at work and stay elected.

If it looks like a deal cannot be agreed before the end of Q1 2019, we would expect sterling to weaken. However, at that stage the Conservative party may decide to issue a series of business tax cuts specifically designed to help Britain survive in a low tax world.

A stable judiciary and legal system created over 300 years ago could mean that the UK may even become the next big offshore Centre, with its own straightforward set of regulations.

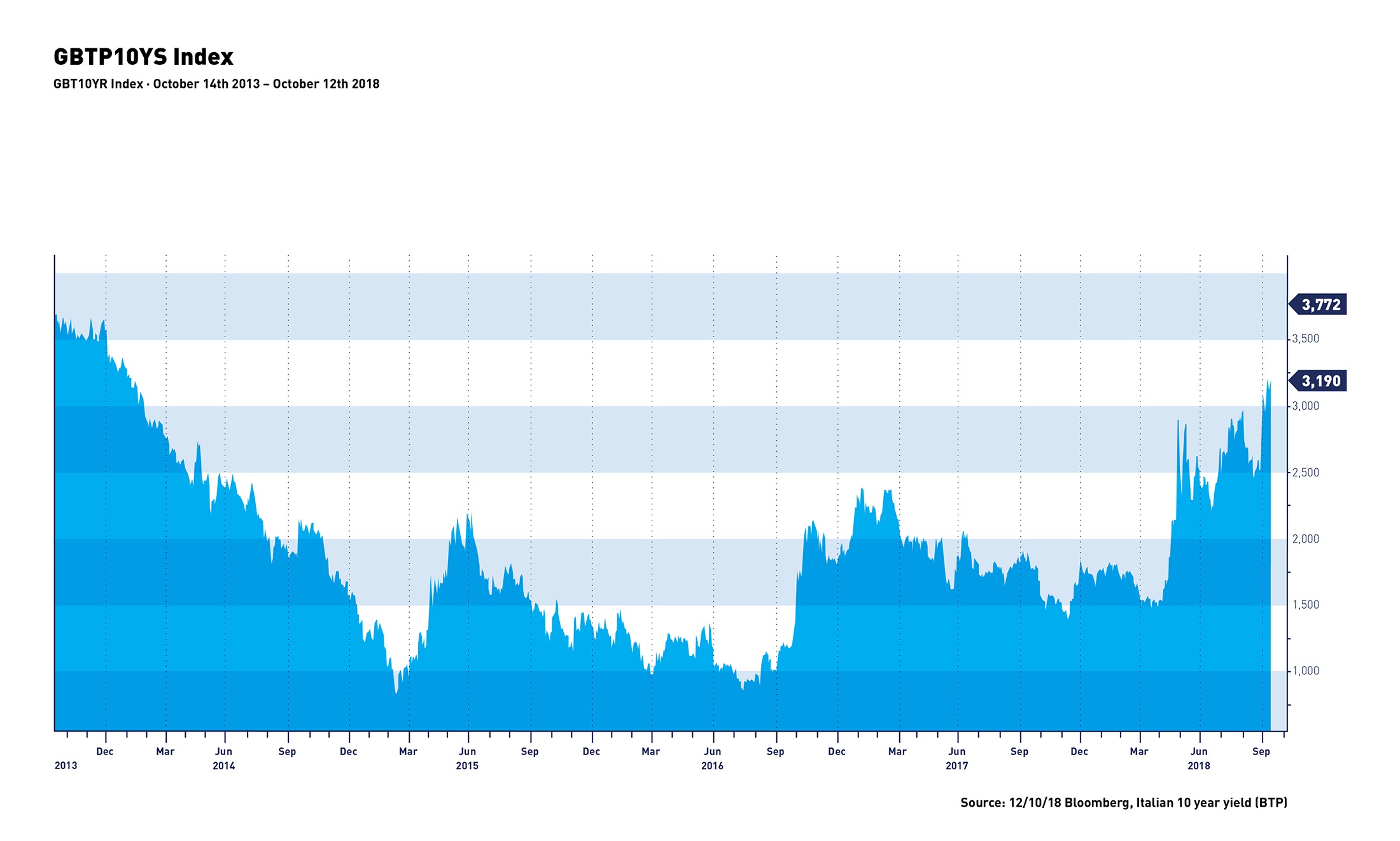

The new populist political parties in Italy are spoiling for a fight with the European club. Following, several years of low consumer confidence and jobs growth, Italy wishes to loosen fiscal constraints in order to boost spending patterns.

As usual, the EU is pushing back on such reforms, as they are mindful that such moves can easily send European Bond yields higher. The move by Italy is important for investors as it could embolden other countries who feel that it is time to try something new.

At the end of the day, such measures are completely understandable, especially given the very poor employment prospects for under 25’s in Italy, many of whom have opted to work in London and elsewhere in recent years. However, as usual, the bond market may have the final say and most politicians will have noticed the rising bond yields in Italian debt markets of late – as a warning sign.

Elsewhere, perhaps as a sign that US credit markets are tightening a little, Goldman Sachs recently announced plans to scale back its unsecured lending to Consumers. In the last 2 years, the firm has built over $4bn in revenues but perhaps senses that as rates rise American consumers may feel the pinch in 2019.

As equity markets fell during October, it seems clear that the market is looking to re-test several key technical support levels. In the financial press, commentators have been quick to highlight fund managers which have made consistent gains in recent years by combining various growth and momentum filters.

In the case of the latter, this frequently involves looking for companies where the share price moves higher and the profit upgrades keep coming. They tend to couple this with a good understanding of the technical support levels and of course, the PE ratio is still for many a deciding factor in stock selection.

From reading through the various data points in the equity markets, it seems that some of the most successful investors are starting to question whether ever-increasing PE ratios can be justified, even when supported by strong growth. In simple terms in some sectors, some PE’s and even PEG ratios (Price Earnings to Growth) are comfortably above their 10 year ranges.

In our view, it may make more sense for the market to scale back on its expectations that certain groups will grow forever and focus on the deviation from the long-term averages.

Written by:

Alan Kinnaird | Senior Portfolio Manager, Partner

Your Wealth at a Glance.

{kind=link}

{kind=link}